Strategic Review Financial Review

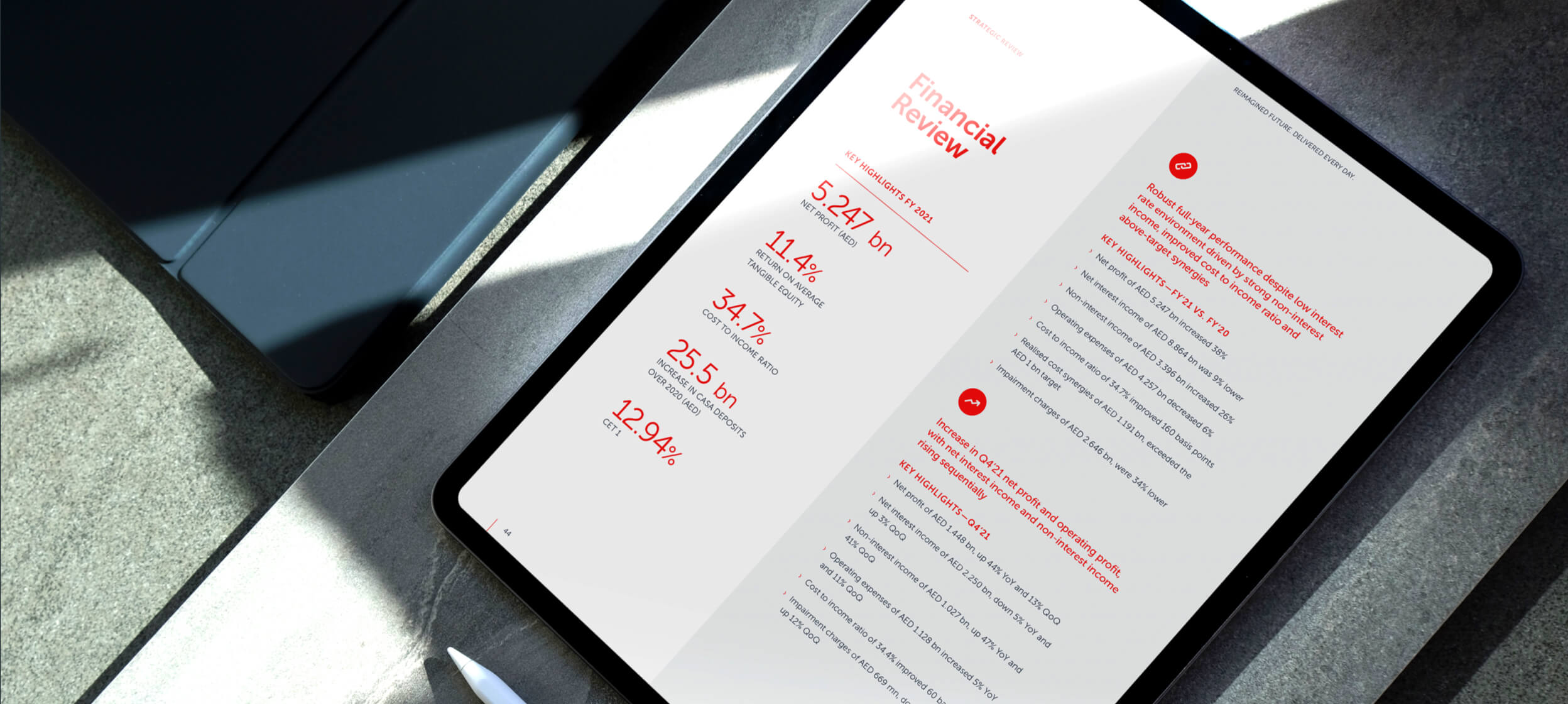

Key Highlights FY 2021

5.247 bn

Net profit (AED)

11.4%

Return on average tangible equity

34.7%

Cost to income ratio

25.5 bn

Increase in CASA deposits

over 2020 (AED)

12.94%

CET 1 ratio

Q4/FY 2021 Financial Highlights

Figures may not add up due to rounding differences

- Operating expenses include non-recurring expenses pertaining to integration-related costs

- After share in profit of associates, overseas income tax charge, and profit/loss from discontinued operations

- Provisions on loans and advances, including fair value adjustments

- POCI: Purchase or originated credit-impaired financial assets

ROBUST FULL-YEAR PERFORMANCE DESPITE LOW INTEREST RATE ENVIRONMENT DRIVEN BY STRONG NON-INTEREST INCOME, IMPROVED COST TO INCOME RATIO AND ABOVE-TARGET SYNERGIES

KEY HIGHLIGHTS — FY’21 VS. FY’20

- Net profit of AED 5.247 bn increased 38%

- Net interest income of AED 8.864 bn was 9% lower

- Non-interest income of AED 3.396 bn increased 26%

- Operating expenses of AED 4.257 bn decreased 6%

- Cost to income ratio of 34.7% improved 160 basis points

- Realised cost synergies of AED 1.191 bn, exceeded the AED 1 bn target

- Impairment charges of AED 2.646 bn, were 34% lower

- Figures may not add up due to rounding differences

INCREASE IN Q4’21 NET PROFIT AND OPERATING PROFIT, WITH NET INTEREST INCOME AND NON-INTEREST INCOME RISING SEQUENTIALLY

Key highlights – Q4’21

- Net profit of AED 1.448 bn, up 44% YoY and 13% QoQ

- Net interest income of AED 2.250 bn, down 5% YoY and up 3% QoQ

- Non-interest income of AED 1.027 bn, up 47% YoY and 41% QoQ

- Operating expenses of AED 1.128 bn increased 5% YoY and 11% QoQ

- Cost to income ratio of 34.4% improved 60 basis points YoY

- Impairment charges of AED 669 mn, down 29% YoY and up 12% QoQ

CREDIT GROWTH OUTPERFORMED BANKING SECTOR DESPITE LARGE CORPORATE REPAYMENTS, SIGNIFICANT RISE IN CASA DEPOSITS

(All numbers are as at 31 December 2021 unless otherwise stated)

- CASA (Current and Savings Account) deposits of AED 153 bn, up AED 25.5 bn during 2021 and AED 6.6 bn sequentially, comprised 58% of total customer deposits (vs. 51% in Dec’20)

- Total customer deposits of AED 265.1 bn were up 3.6% QoQ and 5.4% higher than in Dec’20

- Net loans of AED 244.3 bn were 1.0% higher QoQ and up 2.2% from Dec’20, outperforming the UAE banking sector’s average growth of 0.5% up to the end of November 2021. Including loans to banks, net loan growth was 6.2% in 2021

- Capital adequacy (Basel III) and CET 1 ratios were 15.97% and 12.94% respectively

- Liquidity coverage ratio (LCR) of 124.1%

- Cost of risk was 0.77% in FY’21. NPL ratio was at 5.41% (6.87% including POCI), while provision coverage ratio was 93.4% (149% including collateral held)

The Board of Directors has recommended a cash dividend of AED 0.37 per share¹, translating to a pay-out of AED 2.574 billion, equivalent to 49% of net profit.

- Subject to approval by shareholders at the Annual General Meeting

Key Highlights

FY’21 NET PROFIT UP 38% DRIVEN BY HIGHER NON-INTEREST INCOME, LOWER COST OF RISK AND EFFICIENCIES, WITH SYNERGIES WELL ABOVE TARGET

- Net interest income in Q4’21 increased 3% sequentially to AED 2.250 billion due to higher interest in suspense reversals, and was at AED 8.864 billion in FY’21, a decrease of 9% YoY mainly due to lower benchmark interest rates. Net interest margin (NIM) increased 3 bps sequentially to 2.37% in Q4’21 and was 34 bps lower YoY at 2.43% for FY’21. However, risk-adjusted NIM improved by 30 bps YoY to 1.69% in FY’21, reflecting the change in profile of the loan portfolio. Cost of funds in FY’21 improved by 65 bps to 0.69% as the Bank continued to rebalance its liabilities towards CASA deposits while reducing time deposits.

- The Bank benefitted from growth of diversified revenue streams, with FY’21 non-interest income increasing 26% to AED 3.396 billion, representing 28% of operating income versus 22% the previous year. Net fees and commission income of AED 1.899 billion in FY’21 was up 22%, mainly attributable to a 50% increase in card-related fees and a 27% rise in loan processing fees. Q4’21 non-interest income increased 41% sequentially and 47% YoY to AED 1.027 billion.

- ADCB recorded a gain of AED 166 million during FY’21 on the acquisition of the mortgage portfolio from Abu Dhabi Finance (ADF). This contributed to a 29% YoY increase in other operating income to AED 809 million in FY’21.

- The Bank’s focus on operational efficiency resulted in a 6% reduction in operating expenses to AED 4.257 billion in FY’21. Cost to income ratio improved 160 bps to 34.7% in FY’21, despite the 21% decrease in gross interest income mainly due to lower interest rates. Operating expenses in Q4’21 were AED 1.128 billion, up 11% sequentially and 5% YoY, mainly on account of higher accruals for compensation costs, reflecting strong performance and continued investment in growth of the business.

- The Bank has surpassed its final cost synergy target of AED 1 billion by a significant margin, realising a total of AED 1.2 billion of synergies in FY’21, including AED 207 million in Q4’21.

- The Group reported net profit of AED 5.247 billion in FY’21, up 38% YoY, and AED 1.448 billion in Q4’21, an increase of 13% QoQ and 44% YoY. Return on average tangible equity was 11.4% for FY’21 and 12.6% for Q4’21.

THE BANK EXTENDED AED 40 billion IN NEW CREDIT IN 2021 AND REBALANCED ITS PORTFOLIO, WHILE THE STRONG ADCB FRANCHISE CONTINUED TO ATTRACT CASA DEPOSITS

- The Group’s balance sheet remains strong, with total assets of AED 440 billion as at December-end, up 7% from a year earlier.

- Despite the subdued macro-economic conditions, ADCB capitalised on an active lending pipeline and extended AED 40 billion to targeted economic sectors during 2021, in line with our five-year growth strategy. Corporate repayments of AED 36 billion contributed to a reduction in concentration risk in sectors such as real estate. The consequent healthy net loan growth of 2.2% in 2021 and 1% sequentially to AED 244 billion as at December-end outperformed the UAE banking sector’s average growth of 0.5% up to the end of November 2021. Including loans to banks, net loan growth was 6.2% in 2021. The average customer loan balance for the year was AED 236 billion.

- The rebalancing of the portfolio has resulted in loans to the government and public sector increasing to 26% of gross loans at December-end from 21% a year earlier, while exposure to the real estate sector decreased to 24% from 29% a year earlier.

- Total customer deposits stood at AED 265 billion as at December-end, up 5% year on year and 4% sequentially, compared to system-wide deposit growth of 4.4% to November-end. The Bank continued to optimise cost of funds, attracting AED 25.5 billion of CASA deposits during the year and AED 6.6 billion in Q4’21. CASA deposits totaled AED 153 billion as at December-end, accounting for 58% of total customer deposits, compared to 51% in December 2020. The average deposit balance was AED 249 billion in 2021.

- Others include: Energy, Transport & Communication, Manufacturing, Services and others

- Total shareholders’ equity stood at AED 59 billion as at 31 December 2021, up 5% from a year earlier, after accounting for retained earnings and the proposed dividend payout for 2021.

- The Bank remains well capitalised, with capital adequacy (Basel III) and CET1 ratios of 15.97% and 12.94% respectively as at 31 December 2021, versus 16.61% and 13.30% at the end of 2020. The decrease reflects the proposed 2021 dividends deducted from the capital at year-end, combined with a change in UAE Central Bank regulations that led to an increase in risk-weighted assets.

- ADCB continues to maintain a comfortable liquidity position, with a liquidity coverage ratio (LCR) of 124.1% as at 31 December 2021, while the liquidity ratio stood at 31.2% and the loan to deposit ratio was 92.2%. The Bank was a net lender of AED 16 billion in the interbank markets as at December-end.

SIGNIFICANT IMPROVEMENT IN COST OF RISK IN LINE WITH GUIDANCE; SUCCESSFUL DELIVERY OF TESS PROGRAMME AND NMC RESTRUCTURING

- Cost of risk halved to 0.77% for FY’21 from 1.45% in the previous year, and was 0.70% in Q4’21, in line with medium-term guidance of 0.80%.

- Net impairment charges in FY’21 were 34% lower at AED 2.646 billion, primarily on account of provisioning related to NMC and associated companies recorded in the previous year. In Q4’21 impairment charges were AED 669 million, 29% lower YoY, and were up 12% QoQ mainly on account of a few corporate accounts.

- The NPL ratio decreased to 5.41% at the end of December from 6.04% a year earlier, while the provision coverage ratio was 93.4%, versus 94.3% as at 31 December 2020. The coverage ratio including collateral held was 149% compared to 151% a year earlier. Including net POCI (purchase or originated credit impaired) assets, the NPL ratio was 6.87%.

- During 2021, ADCB continued to provide support, including loan deferrals, to individuals, SMEs and corporates impacted by the global pandemic. Active engagement resulted in a large majority of customers resuming repayments or agreeing long-term solutions.

- Following expiry of the UAE Central Bank’s TESS loan deferral programme at the end of 2021, ADCB has resumed full application of normal classifications for SICR (significant increase in credit risk) and staging rules, and no longer provides TESS deferrals. Meanwhile, a TESS ‘recovery programme’, under the auspices of the UAE Central Bank, continues to allow banks to extend new loans to customers who have temporarily lost revenue due to Covid-19, but are otherwise in good economic health. Employing its usual internal credit policies and underwriting processes, ADCB has provided a total of AED 873 million of loans under the programme, of which AED 219 million has been repaid.

ADCB EXPECTED TO RECEIVE C. 38% OF EXIT INSTRUMENTS IN A NEW USD 2.25 billion FACILITY AS NMC GROUP IS SCHEDULED TO EXIT ADMINISTRATION IN Q1’22

- On 1 September 2021, NMC Group creditors voted overwhelmingly in favour of a debt restructuring plan and the exit of the Group from administration via deeds of company arrangement (DOCA), which is scheduled for Q1’22.

- Creditors, including ADCB, will receive ‘exit instruments’ in a USD 2.25 billion ‘Holdco facility’, a debt claim sized to the expected future value of NMC Group. All net proceeds from a future sale of the business will return to holders of exit instruments, including any value in excess of USD 2.25 billion. There are also further possibilities to benefit from potential recoveries from the company’s ongoing litigation. Participants in exit instruments will receive a cash margin of 0.5% per annum, as well as payment in kind of 2% per annum (paid along with principal), which will accrue from the date of the signing of the facility document.

- ADCB is expected to receive approximately 38% of the transferable exit instruments. The Bank participated in a USD 325 million ‘Administration Funding Facility’ (AFF), which granted elevation and conversion rights in the new Holdco Facility. The AFF is expected to be repaid using proceeds from the sale of non-core assets of NMC Group.

- Given this material progress in restructuring, the Bank considers the provisions and interest in suspense for NMC Group recorded to date to be at an appropriate level at AED 1.142 billion as at 31 December 2021.

- ADCB will appoint three of the seven non-executive directors that participants in the exit instruments will select to the new Holdco’s Board of Directors. The restructuring enables NMC Group to create maximum value for its creditors while ensuring operational continuity for patients, healthcare workers and other stakeholders.

DIGITAL TRANSFORMATION DELIVERING STRONG RESULTS, WITH ONBOARDING APP LEADING THE MARKET AND MOBILE BANKING SUBSCRIBERS UP 27% IN 2021

- Digital transformation is at the core of ADCB Group’s five-year strategy, powering enhancements to Consumer and Wholesale Banking platforms, greater customer engagement and operational efficiencies. In 2021, registrations for the ADCB Mobile Banking App climbed 27% to surpass 860,000 customers, while the total number of subscribers to digital platforms has reached 989,000. As of January 2022, digital registrations have exceeded a key milestone of 1 million customers subscribed.

- In 2021, 95% of retail transactions were conducted electronically and digital fund transfers increased 73% YoY. Transactions on Wholesale Banking’s ProCash and ProTrade platforms accounted for 96% of all cash management transactions and 74% of trade finance transactions respectively.

- The Bank’s onboarding app ‘Hayyak’, registered over 165,000 new customers in 2021, representing 76% of the total.

- ADCB launched a further seven digital customer releases in Q4’21, taking the total to 93 since the inception of the digital transformation programme. Key initiatives included introduction of WhatsApp banking, which offers convenient and secure customer service, as well as a series of self-service capabilities on Wholesale Banking platforms, additional security features on ProCash mobile and automated statement analysis for SMEs.

DIGITAL PROGRESS DRIVES GROWTH AT AL HILAL BANK AND ADCB EGYPT

- ADCB Egypt delivered a strong performance in 2021, expanding its customer base and significantly increasing loans and deposits. The Bank’s growth was underpinned by the introduction of a digital transformation programme, which has enhanced internal systems and processes, upskilled employees, and digitalised over 100 services. This has resulted in a significant increase in the number of active subscribers to digital platforms, with 51% of transfers and payments conducted digitally. The Bank has broadened its range of products and services, including the introduction of an ‘Excellency’ segment and premium credit cards aimed at affluent customers.

413 mn

FY’21 net profit¹ (EGP)

+32% YoY, representing an ROE of 9.07%

21 bn

Net loans (EGP)

+28% in 2021, as at 31 December 2021

41 bn

Total deposits (EGP)

+42% in 2021, as at 31 December 2021

- Based on IFRS

- Al Hilal Bank is making strong progress in its strategy to be a fully digital Shari’ah-compliant bank focused on providing retail customers with a differentiated offering that goes well beyond traditional banking services. The Bank is set to launch a new cloud-based digital platform that will offer financial solutions and a wide range of other services through an ecosystem of partnerships. The value proposition has received positive feedback during testing by a community of potential customers. The new platform builds on a track record of increasing digital engagement, with active users of Al Hilal Bank’s digital platforms increasing by 43% during 2021, and registered subscribers increasing 47%.

GROWING BASE OF EMIRATI TALENT, NURTURED THROUGH MARKET-LEADING TRAINING AND PROFESSIONAL ADVANCEMENT OPPORTUNITIES

- ADCB’s learning programme, opportunities for professional advancement, and a highly engaged workplace have established ADCB as a top choice for UAE nationals pursuing a rewarding career. Attracting and developing UAE national talent is a key strategic objective and provides the Bank with a strong competitive advantage as the country presses ahead with initiatives to create skilled jobs.

- ADCB continues to honour its commitment to Emiratisation. In 2021, the Bank recruited 477 UAE nationals. The total number of Emirati staff at the ADCB Group reached a total of 1,854, representing 18% of Emiratis employed in the UAE banking sector.

- UAE nationals represent 38% of employees at ADCB and 51% at Al Hilal Bank, which is amongst the highest Emiratisation rates in the UAE banking sector. Emiratis hold 30% of senior leadership positions at ADCB Group. Female Emiratis account for 50% of UAE nationals in senior and middle management positions.

- Over 40% of the Group’s Emirati employees started their career at the Bank, benefitting from a comprehensive career development programme. More than 105,000 hours of training were delivered in 2021 to Emirati employees, and 150,000 hours are planned for 2022.