Letters spacing

Letters spacing Line height

Line height Default

Default Big

Big More big

More big Default

Default Black & White

Black & White

Money Guide for Expatriates in the UAE Financial flexibility for unforeseen circumstances

srchThumbnail:/en/Images/financial-resilience-200x200_tcm41-563035.webp

Life is full of surprises, often unpredictable and sometimes financially challenging. Unplanned financial events can strike at any time, disrupting even the most carefully managed budgets and causing significant stress. Fortunately, recent years have seen a growing awareness of financial planning, supported by various government initiatives. Explore how to achieve financial resilience and achieve peace of mind.

Key insights

Recent surveys and insights into the UAE’s financial landscape reveal a mix of optimism and concern as highlighted in the following findings:

UAE Money Report 2025 by Zurich Middle East UAE

- 68% of people in the UAE feel confident about their financial situation, though many still face challenges.

- 75% of citizens and residents are confident they have sufficient funds for retirement.

- 27% of people plan to invest in building skills such as AI.

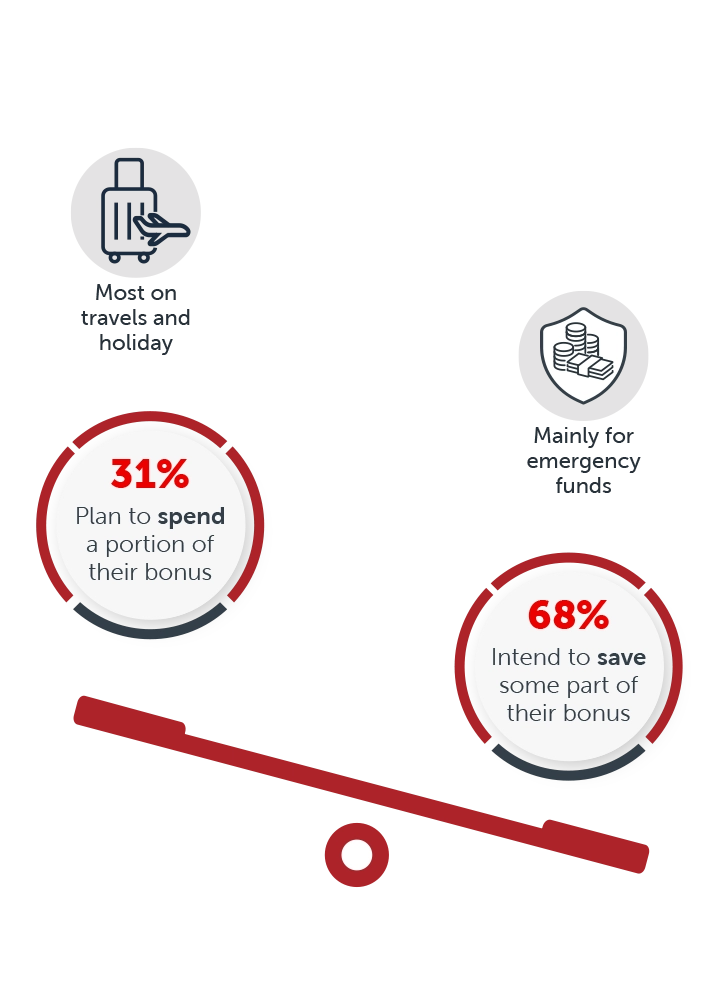

- 75% of respondents expect a windfall or bonus in 2025. Of these, 68% intend to save some part of their bonus while 31% plan to spend a portion of it.

- 31% of Gen Z plans to save their entire bonus, 63% of Millennials aim to save most of their bonuses and 52% of individuals aged 45 and above intend to save majority of their windfall rather than spend it all.

Not saving enough by International Financial Group Limited (IFGL)

- 53% of respondents cited “not saving enough” as their top concern followed by 49% worried about “paying rent”, 39% about the “cost of medical insurance” and 32% about “retirement funding.”

- Individuals with higher income (over AED 25,000) are more concerned about retirement funding than those with lower income (under AED 10,000).

- In contrast, UAE residents are relatively unconcerned about financial obligations such as paying for a mortgage (19%), going on a summer holiday (16%) or a child’s wedding (9%).

- Married respondents are significantly more worried about not saving enough and funding retirement.

- The younger age group (18-24 years old) is more concerned about their savings level than any other age group surveyed.

Common disruptions

These are typically the scenarios which cause a significant dent in the budget:

- Vehicle issues

- Sudden breakdowns which would require repairs

- Unexpected fines or registration costs

- Unplanned car rentals

- Housing costs

- Increase in rent or possible relocation

- Security deposit for a new flat

- Urgent home repairs

- Family emergencies

- Unplanned travel requirements

- Renewal of visa or cancellation fees

- Urgent remittance to support loved ones

- Medical emergencies

- Out-of-pocket costs for dental or optical works

- Visits to specialists

- Prescriptions not covered by insurance

- School needs

- Tuition fees, adjustments to the tuition or exam fees

- School project materials

- Extracurricular activities like field trips

- Device failures

- Replacement of broken device/s used for work or school

- Repair services or recovery of data

- Social and cultural obligations

- Weddings, birthdays or religious events

- Attending community gatherings

Building financial resilience

- Create an emergency fund:

As cliché as it may sound, having a fund tucked away for such emergency scenarios is a lifesaver. Starting an emergency fund will depend on many factors and the individual’s circumstances. The aim is to save 3-6 months of essential expenses. You can start with a small goal of AED3,000 and gradually build the fund. Goal-based savings account is also a great way to start.

Determining the right size of your emergency fund:- If you have a low maintenance lifestyle and have sufficient savings as a buffer, 3 months’ worth of savings is sufficient to cover the necessary expenses like rent, groceries, transportation and utilities. Assuming healthcare is covered by insurance.

- If you are paying instalments for loans, paying for credit cards or have dependents, 6-9 months’ worth of emergency fund provides a good cushion to get you through.

- If you frequently face unexpected costs, consider building a larger fund to help you stay on track to minimize the financial shock.

- Automate your savings:

This step may not seem much but it ensures consistency and removes temptation to spend. You can open a separate account and set up automatic transfer to build your fund.

- Choose high interest savings accounts:

UAE banks offer competitive rates that help you grow your savings passively.

- Redirect windfalls:

Bonus, income from side hustle or refunds should go directly to your emergency fund.

- Avoid lifestyle inflation:

It is very tempting to upgrade your lifestyle when your income increases. Resist the impulse and prioritise saving instead.

- Track your spending:

It is easy to forget what and where you spent your hard-earned money on. Tracking your spending will allow you to identify areas and to cut down unnecessary costs and more opportunities to save. Choose from the numerous budgeting apps online or if you want to keep it analog, you can create excel spreadsheets.

Government support

The UAE government has introduced the Involuntary Loss of Employment (ILOE) insurance scheme to support residents in the event of job loss. The initiative provides a crucial safety net and encourages proactive financial planning.

Financial stability is not just about numbers, it is about peace of mind, security and the ability to care for loved ones when life takes an unexpected turn. Whether it is a sudden expense or a change in circumstances, being prepared can make all the difference. Every dirham saved is a step toward a more secure future and there is no better time to start than today.