Letters spacing

Letters spacing Line height

Line height Default

Default Big

Big More big

More big Default

Default Black & White

Black & White

Building Wealth Stocks versus Bonds: Two pillars of investing

srchThumbnail:/en/Images/comparing-stocks-and-bonds-200x200_tcm41-564756.webp

The core of investing: How stocks and bonds shape your financial future

At its heart, investing is about channelling resources to generate returns over time and create wealth. While there’s a wide array of financial instruments available, stocks and bonds stand out as two foundational pillars of investing. They both play distinct roles in investment strategy, offering different forms of return and risk in a portfolio. Understanding their characteristics, advantages, and limitations is central to making informed financial decisions, to help reach your financial goals.

Stocks: The growth driver

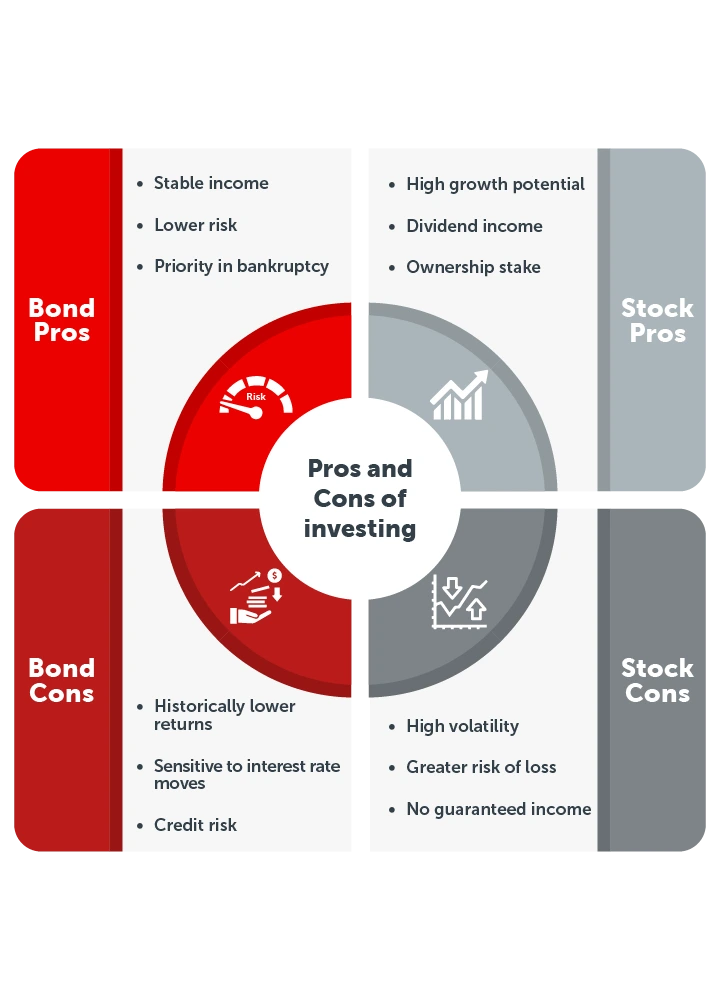

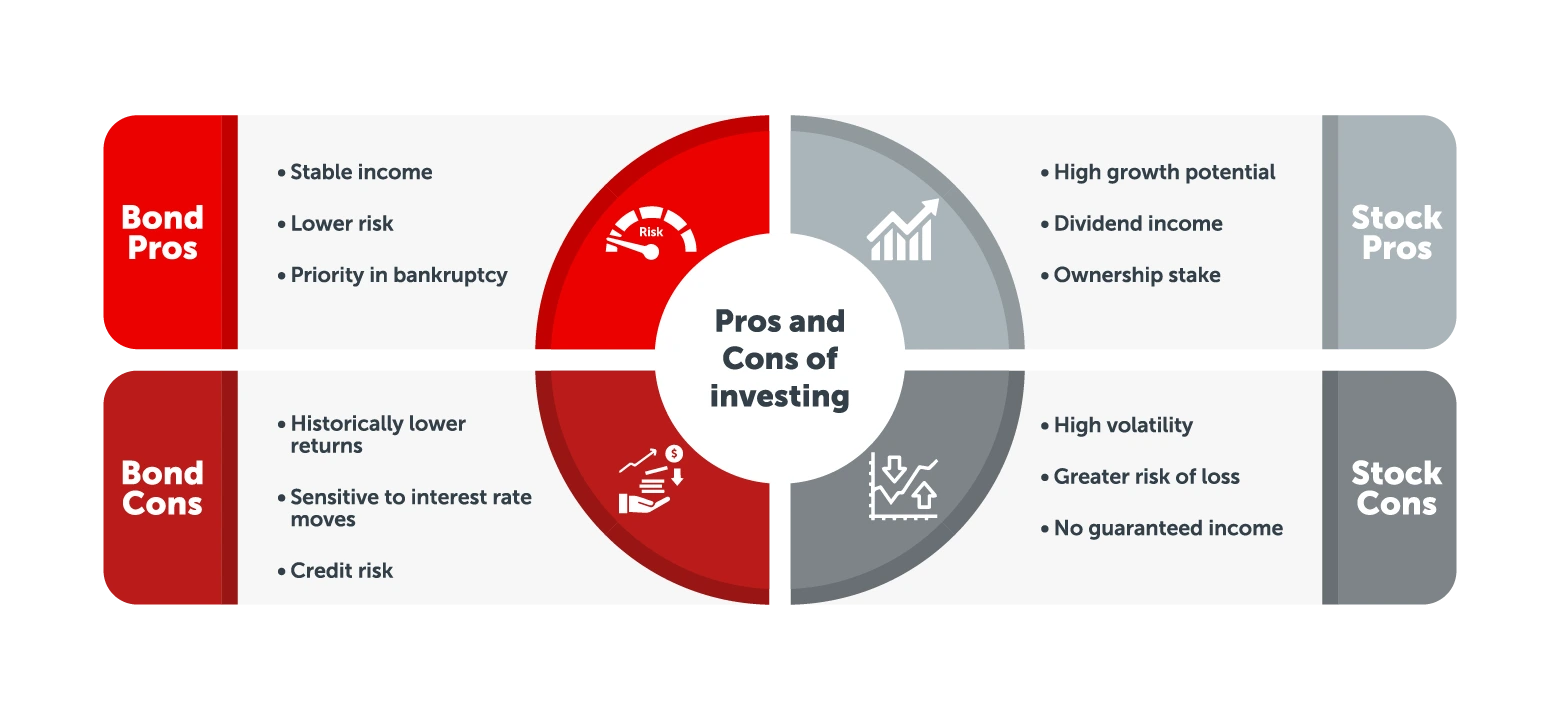

Stocks, or equities, represent partial ownership in a company. When an investor purchases a stock, they acquire a stake in the company’s future profits and, in some cases, a say (voting rights) on corporate strategy. Stock returns are often generated in two main ways: capital appreciation, when the market value of shares rises and dividends, which are periodic payments made from company profits. It’s important to note that not all companies offer dividends.

Stocks’ primary appeal is their growth potential. Some regional and global companies have had a steady track record of capital appreciation and regular dividends that have made them attractive investments over the years.

Key takeaway

Stocks offer long-term growth potential through capital appreciation and dividends, but they come with higher volatility. They’re best suited for investors who can tolerate risk and focus on long-term wealth building.

Indeed, over extended periods, equities have historically outperformed many other asset classes, including bonds, allowing investors to build significant wealth. However, there’s a catch: stocks are inherently more volatile. Prices fluctuate with changes in company performance, economic conditions, geopolitical events, and shifting investor sentiment. This volatility means that the flip side of high reward is the greater likelihood of short-term losses compared to more stable investments, such as bonds.

Equities are particularly suitable for long-term investors who can tolerate market swings and are focused on capital growth over multiple years or decades. They are also a tool for participating in sectors or companies that are driving innovation, infrastructure, or industrial development globally. The recent rally among big tech companies in the United States driven by the promise of artificial intelligence, is a case in point.

Bonds: The portfolio stabiliser

Bonds offer a contrasting investment experience. When an investor buys a bond, they are lending money to an issuer, whether it’s a government, company, or organisation, in exchange for regular interest payments called coupons and the return of principal at the end of the bond’s term. Because of this fixed-income structure, bonds are generally regarded as less risky than stocks, providing a more predictable stream of income.

The risk profile of bonds depends on factors such as the issuer’s creditworthiness, interest rate movements, and inflation. Government bonds issued by financially stable countries tend to carry lower risk, while corporate bonds may offer higher yields to compensate for increased risk. Importantly, bond values move inversely with interest rates: when rates rise, bond prices fall and vice versa. Investors must also consider inflation risk, as rising prices can erode the real value of fixed interest payments.

Bonds are often used to preserve capital and provide a steady income stream. They serve to offset stock volatility, helping investors navigate market uncertainty with more predictable and stable returns.

Both play complementary roles in a portfolio

Stocks and bonds are not competitors; rather, they complement each other in a diversified portfolio. Equities offer growth and the potential to outpace inflation, while bonds provide stability and predictable returns. By holding both asset types, investors can balance the trade-off between risk and reward.

The allocation between stocks and bonds typically depends on individual goals, risk tolerance, and investment horizon. Younger investors or those with a longer time frame may benefit from greater exposure to equities to maximise growth potential as they have time to recover from short-term market volatility. Conversely, investors near retirement or seeking income stability may prioritise bonds to reduce exposure to market volatility. Many investment strategies use dynamic allocation, adjusting the balance of stocks and bonds over time to match changing financial objectives and market conditions.

Global context and diversification

Across domestic, regional and global markets, stocks and bonds remain foundational to wealth-building and institutional investing. Stocks allow participation in economic expansion, innovation, and industrial growth, while bonds provide predictable funding mechanisms for governments and corporations. Investors can also diversify across geographies, sectors, and types of bonds (government, corporate, or supranational), enhancing portfolio resilience.

For instance, investors can combine domestic and international equities to capture growth in emerging markets or developed economies, while holding bonds denominated in different currencies or with varying maturities to manage risk. This diversification helps mitigate the impact of localised economic shocks or sector-specific volatility.

It's also about gaining access. While equities are more popular among Gulf investors, several financial institutions offer bond mutual funds and exchange trade funds to give retail and institutional investors exposure to domestic and regional bond instruments.

Key takeaway

Stocks and bonds are essential tools for building diversified portfolios. While stocks offer growth through economic participation, bonds provide stability and income. Combining both across markets and sectors enhances resilience and access to broader investment opportunities.

What investors should consider when investing

Investors should consult with their financial advisors or do their own research to get answers on the following:- What’s my risk tolerance?

How much volatility can be managed without triggering premature selling? - What’s my time horizon?

Longer-term horizons favour equities; shorter-term horizons benefit from the stability of bonds. - What are my income requirements?

Bonds may be prioritized for regular cash flow, stocks for reinvested growth. - What’s the market outlook?

Inflation, interest rates and economic cycles affect both asset types differently.

Answers to these questions can help investors craft a portfolio tailored to their objectives, risk appetite and time horizon.

Glossary

For Glossary of terms, abbreviations and explanations on investments, please visit adcb.com/invglossary.

Wealth Management solutions

Discover reliable, innovative Wealth Management solutions. Learn more.

Disclaimer

ADCB’s products and services are subject to Consumer Banking Terms and Conditions. Abu Dhabi Commercial Bank PJSC ("ADCB", "The Bank") is licensed by the Central Bank of the United Arab Emirates under license number 13/2461/2005 to provide banking services to its clients and by the Securities and Commodities Authority to promote investment securities and provide investment related services under license number 601001.

This webpage is for information and illustrative purposes only and does not constitute any form of advice, commitment or engagement on behalf of the Abu Dhabi Commercial Bank and any of its subsidiaries including ADCB Asset Management Limited ("ADCB Group"). It should not be construed as an offer or solicitation to buy or sell any investment products, nor is it to be considered as personalised investment advice. It should be read in conjunction with applicable documents and respective terms and conditions for potential investor to understand the terms and information contained therein. Persons receiving this email are instructed to discuss it with their professional legal, financial and tax advisors before they make any financial commitments and shall be deemed to have made a reasonable assessment of the potential risks and rewards in making such a commitment. ADCB Group does not guarantee any third party service provider, and investors invest at their own risk and bear all risks involved in any product purchased. ADCB Group will not hold any responsibility for the outcome of any investment decisions taken. Past performance does not guarantee future results. Investment products are not Bank deposits and are not guaranteed by the ADCB Group, they are subject to investment risks, including possible loss of the principal amount invested. Please refer to ADCB Wealth Services Terms and Conditions and/or to ADCB Asset Management Limited Terms and Conditions.

Did you know?Stocks and bonds play different roles in portfolios

Knowledge quiz What differentiates stocks from bonds?

Tags: Nearing Retirement Entrepreneurs Growing Your Savings Growing Your Business Investing for Growth