Letters spacing

Letters spacing Line height

Line height Default

Default Big

Big More big

More big Default

Default Black & White

Black & White

Building Wealth Sukuk: The debt instrument powering Islamic finance

srchThumbnail:/en/Images/sukuk-cea-200x200_tcm41-564289.webp

The global rise of Sukuk in capital markets

Once considered a niche component of Islamic finance, Sukuk have steadily gained global traction, evolving into a mainstream instrument within international capital markets. Their appeal lies in their ability to offer Shari’ah-compliant investment opportunities while supporting critical funding needs such as infrastructure development, sustainability initiatives and economic diversification.

As investor interest continues to grow, both from Islamic and conventional markets, the total outstanding value of Sukuk is on track to surpass one trillion United States Dollars (USD), marking a significant milestone in the evolution of ethical finance.

Sukuk have emerged as a fiscal debt policy pillar for several Gulf and Southeast Asian countries since their launch in 1990. They have also evolved from a niche Islamic finance product into a core debt-raising tool for many Islamic countries, enabling governments to diversify funding sources, meet budgetary needs and align capital raising with Shari’ah principles that prohibit riba (interest), gharar (excessive uncertainty) and non-permissible activities.

While the global Sukuk market remains concentrated in a handful of jurisdictions, it is broadening geographically and thematically. With continued sovereign diversification, Shari’ah-compliant energy transition financing and technology-driven issuance models, Sukuk are poised to remain a robust segment of global fixed-income markets.

The rise of Sukuk as a fiscal policy lever

Several countries, especially in the Gulf Cooperation Council (GCC), have embraced Sukuk issuance as a strategic funding mechanism to finance infrastructure projects, budget deficits and economic diversification agendas.

Sovereign Sukuk now account for a substantial share of Gulf capital markets, with the United Arab Emirates (UAE)[3] , Saudi Arabia and Qatar issuing Sukuk to tap both domestic and international investors. Sukuk also allow governments to mobilise liquidity from Shari’ah-sensitive capital pools while maintaining compliance with domestic and regional religious frameworks.

By issuing Sukuk alongside conventional bonds, governments in the GCC, Malaysia and Indonesia have built dual-track capital-raising programmes, broadening investor bases and enhancing market depth.

Economic growth and financing needs in Islamic countries have given Sukuk global appeal, attracting conventional investors seeking diversification, particularly in the low-yield environment.

Unlike conventional bonds, which are pure debt instruments paying interest, Sukuk grant investors ownership in assets or projects, generating returns from profits or rent. This structure ensures Shari’ah compliance by avoiding riba (interest), gharar (excessive uncertainty) and prohibited activities.

Sukuk must be underpinned by assets such as government infrastructure, industrial facilities, real estate, or public utilities. The assets must be identifiable and legally transferable in ownership or beneficial rights.

They generally track comparable conventional bonds, adjusted for liquidity, credit quality and investor demand. In certain markets, Sukuk trade at a slight yield premium due to narrower investor bases, but this gap has narrowed in GCC markets.

Sukuk Categories:

- Sovereign Sukuk Issued by governments, often for budget support or infrastructure.

- Corporate Sukuk Issued by companies to finance expansion, refinancing, or projects.

- Private Sukuk Issued to a limited group of investors

Sukuk also have a range of credit structures:

- Tier 1 and Tier 2 Sukuk

Primarily issued by banks to meet Basel III capital adequacy requirements. - Senior Unsecured Sukuk

Ranked equally with other unsecured obligations. - Secured Sukuk

Backed by specific assets, offering added investor protection.

The diverse world of Sukuk issuance

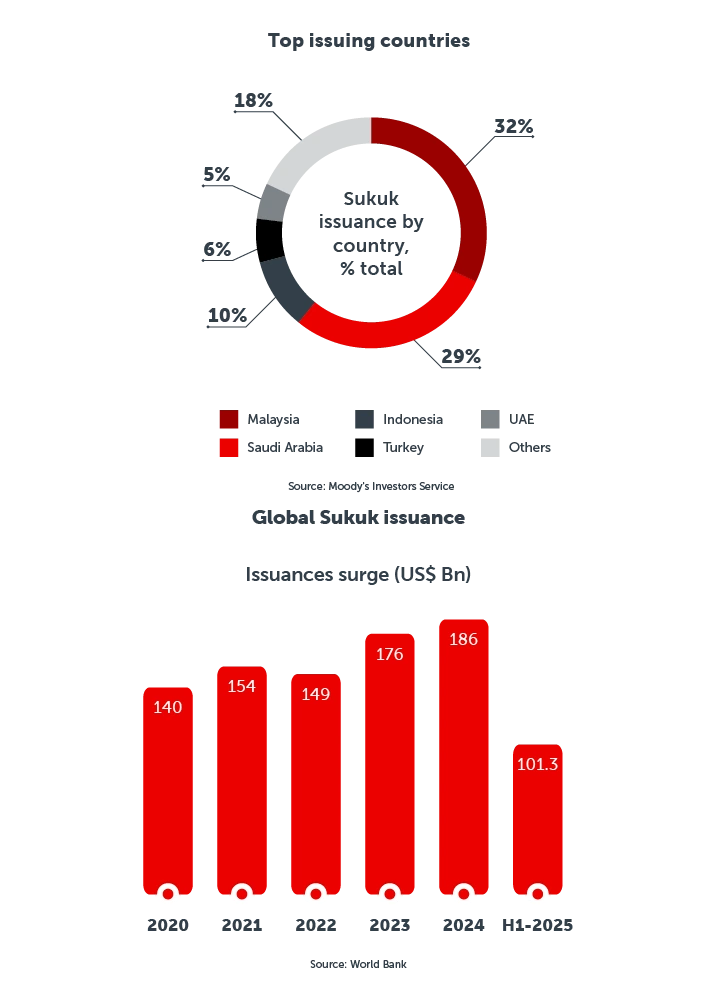

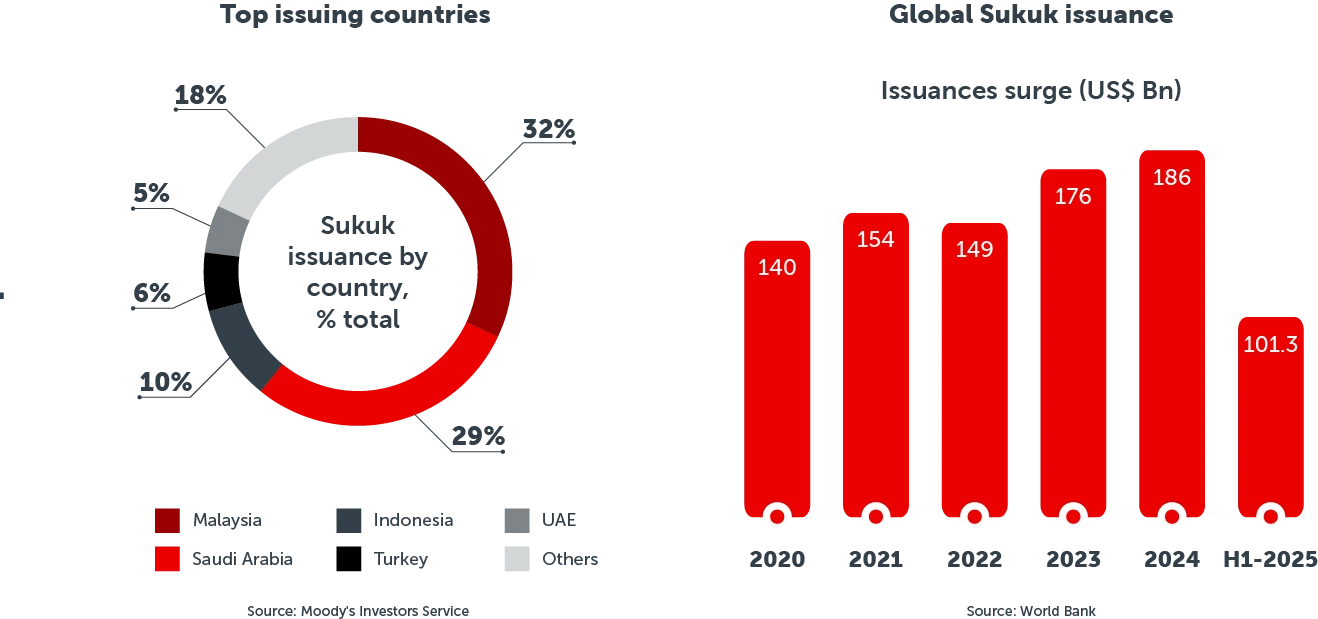

The Sukuk market is concentrated in a few jurisdictions, but each has developed distinct issuance ecosystems. Malaysia has emerged as a global leader in issuance volume, with deep local investor participation and regulatory maturity. Meanwhile, the UAE[3] is active in both sovereign and corporate issuance, positioning itself as an Islamic finance hub.

Saudi Arabia, a G20 nation, is a major issuer of sovereign Sukuk, leveraging strong fiscal needs and domestic liquidity as it pursues an ambitious economic diversification drive. Indonesia, on the other hand, is a pioneer in green Sukuk and retail Sukuk, broadening investor access. Bahrain and Oman also maintain active programmes.

Turkey, Pakistan and the United Kingdom (UK) are among countries that have tapped Sukuk to diversify their funding requirements. By the end of 2024, 21 countries[1] had participated in the Sukuk market.

“The growing number of participating countries underscores the increasing interest and attractiveness of this financial instrument,” according to Cbonds[1] , which is often compared to the global capital market. Additionally, the balanced structure of issuances reflects equal interest from both state-owned entities and corporations, highlighting Sukuk’s broad appeal across different sectors.

Regulatory frameworks and Shari’ah compliance

Sukuk structures vary across jurisdictions due to differing Shari’ah interpretations and legal systems. The differences arise due to diversity of opinion in Shari’ah supervisory boards that approve structures to ensure compliance. In some markets, it is centralised (for example, Malaysia), while in others, approval is decentralised at issuer or bank level.

Differences in the International Financial Reporting Standards (IFRS) and the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) standards can impact asset recognition and investor reporting. In the GCC, Sukuk are typically approved by an Internal Shari’ah Supervisory Committee (ISSC) or an external Shari’ah board. This process ensures contractual terms avoid prohibited elements and that asset transfers are valid under Islamic principles.

Some analysts[2] argue that streamlining issuance processes and standardising Shari’ah guidelines could unlock the Sukuk market’s potential as a globally competitive, inclusive financial instrument.

Bridging ethical investment and green growth

Given their focus on ethical financing and prohibition on engaging in harmful activities, Sukuk are uniquely positioned to align with Environmental, Social and Governance (ESG) or sustainable debt instruments. ESG Sukuk, particularly green Sukuk, are gaining traction in the UAE[3] and Saudi Arabia, especially to finance renewable energy and sustainable infrastructure.

The ESG component has also opened up Sukuk to conventional investors seeking impact-driven investments. That could prove to be significant as the sustainable bond market is expected to surpass USD 1 trillion in 2025, according to Moody’s Investors Service[4] .

Innovation driving Islamic finance forward

- Green Sukuk

Financing renewable projects, energy efficiency upgrades and sustainable transport. - Digital Sukuk

Blockchain-based Sukuk are being explored to enhance transparency, reduce issuance costs and broaden global investor participation. - Retail Sukuk

Especially in Indonesia and Malaysia, these offer Sukuk in smaller denominations to individuals, expanding financial inclusion. - Hybrid Structures

Combining Sukuk tranches with conventional bonds to reach a diverse set of investors.

Sukuks driving diversification and development

Total Sukuk issuance in 2024 stood at around USD 180 billion, with the market set to reach a total outstanding amount of USD 1 trillion[3] in the next few years.

Sukuk will remain a key financing instrument in the fiscal toolbox of several GCC states and other Islamic countries, especially as they continue to diversify their economies. In addition, Sukuk are also emerging as a preferred way to raise energy-transition financing, which could make them attractive in emerging markets beyond the Islamic world. Another key driver in enhancing Sukuk cross-border appeal could be technology adoption and innovation.

Sukuk are expected to maintain a meaningful share of emerging market issuance, having accounted for 12% of all Emerging Markets (EM) US-dollar debt in 2024 (excluding China). The outlook is supported by resilient Islamic investor demand, sovereign diversification agendas, the need to refinance upcoming maturities and funding for government projects and fiscal deficits, underpinned by ongoing debt capital market reforms.

Risks remain, including Shari’ah-compliance complexities, geopolitical tensions, higher oil prices and rising rates. With analysts such as Fitch Ratings[5] forecasting a 100-basis-point Federal Reserve rate cut to 3.5% by the fourth quarter of 2025 (and steady through end-2026), the overall funding backdrop appears constructive, with investment-grade issuers enjoying favourable terms.

Glossary

For Glossary of terms, abbreviations and explanations on investments, please visit adcb.com/invglossary.

Wealth Management solutions

Discover reliable, innovative Wealth Management solutions. Learn more

Disclaimer

ADCB’s products and services are subject to Consumer Banking Terms and Conditions. Abu Dhabi Commercial Bank PJSC ("ADCB", "The Bank") is licensed by the Central Bank of the United Arab Emirates under license number 13/2461/2005 to provide banking services to its clients, and by the Securities and Commodities Authority to promote investment securities and provide investment related services under license number 601001.

This webpage is for information and illustrative purposes only and does not constitute any form of advice, commitment or engagement on behalf of the Abu Dhabi Commercial Bank and any of its subsidiaries including ADCB Asset Management Limited ("ADCB Group"). It should not be construed as an offer or solicitation to buy or sell any investment products, nor is it to be considered as personalized investment advice. It should be read in conjunction with applicable documents and respective terms and conditions for potential investor to understand the terms and information contained therein. Persons receiving this email are instructed to discuss it with their professional legal, financial and tax advisors before they make any financial commitments and shall be deemed to have made a reasonable assessment of the potential risks and rewards in making such a commitment. ADCB Group does not guarantee any third party service provider, and investors invest at their own risk and bear all risks involved in any product purchased. ADCB Group will not hold any responsibility for the outcome of any investment decisions taken. Past performance does not guarantee future results. Investment products are not Bank deposits and are not guaranteed by the ADCB Group, they are subject to investment risks, including possible loss of the principal amount invested. Please refer to ADCB Wealth Services Terms and Conditions and/or to ADCB Asset Management Limited Terms and Conditions.

Did you know?Sukuk as ethical instruments for global investors

Knowledge quiz What distinguishes Sukuks from conventional bonds?

Tags: Nearing Retirement Entrepreneurs Growing Your Savings Growing Your Business Investing for Growth