Letters spacing

Letters spacing Line height

Line height Default

Default Big

Big More big

More big Default

Default Black & White

Black & White

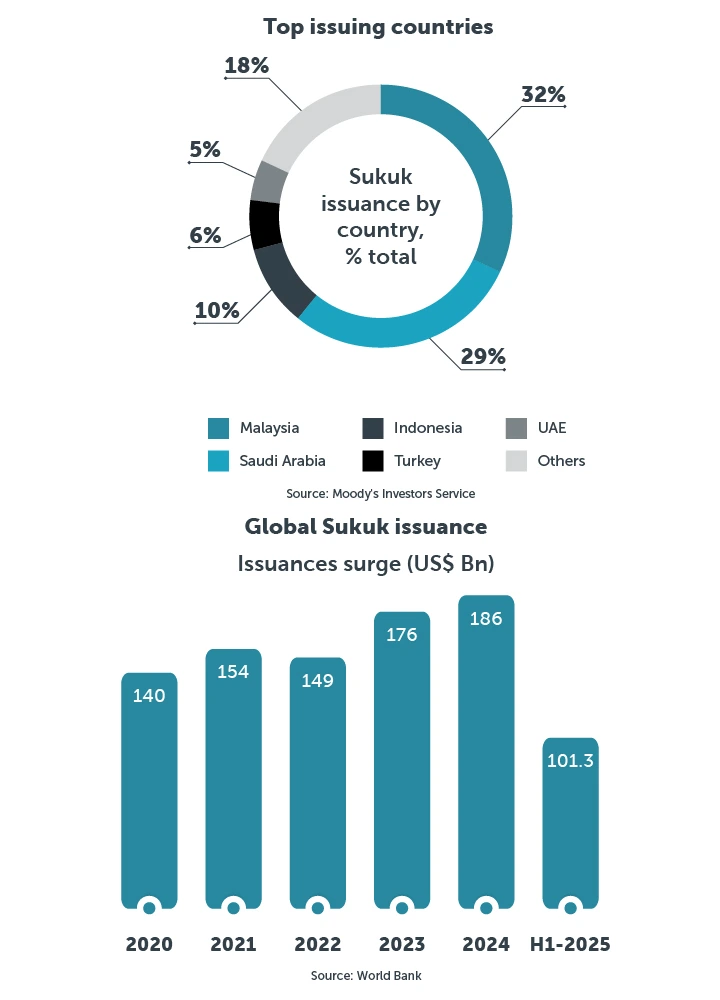

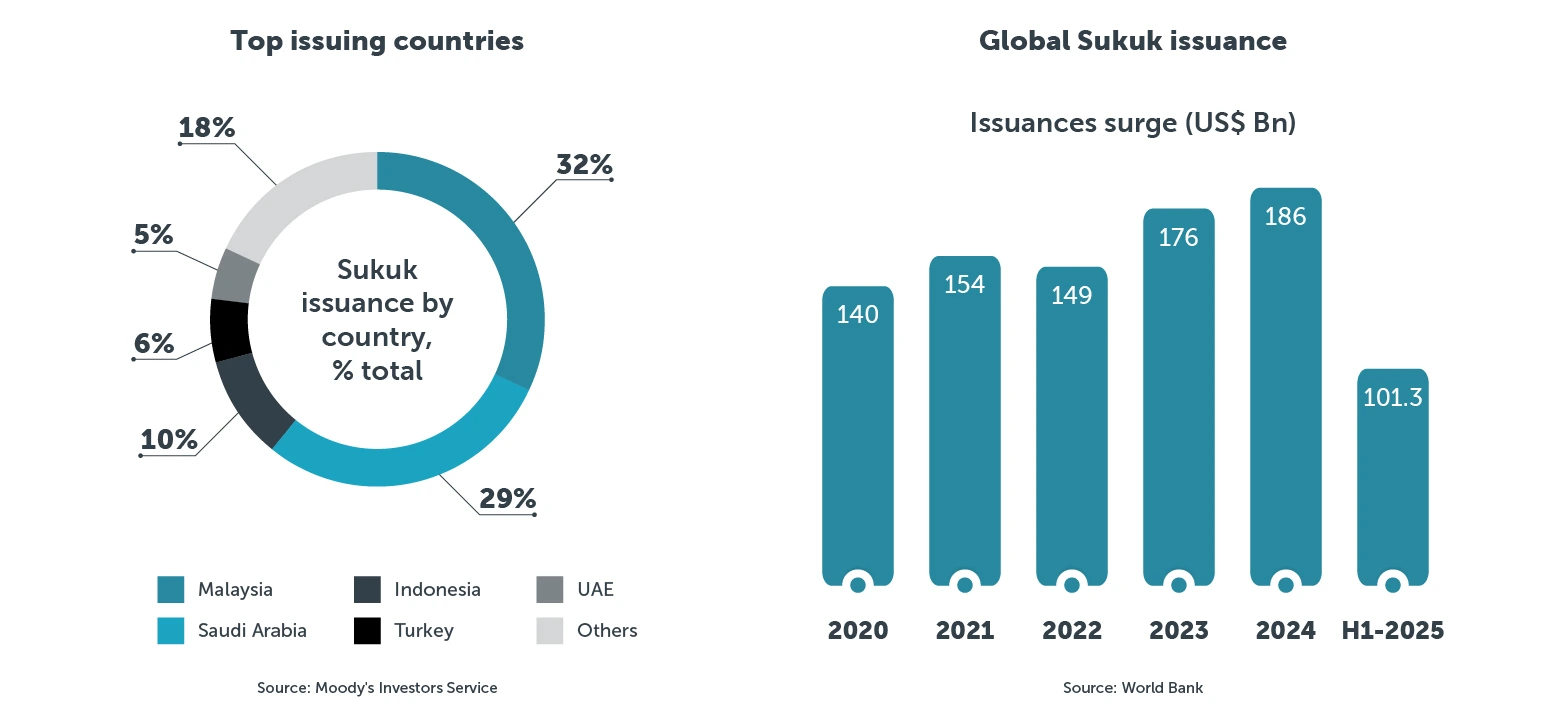

ADCB Islamic Banking All you need to know about Sukuk

srchThumbnail:/en/Images/uncovering-the-global-rise-of-sukuk-200x200_tcm41-564579.webp

A key pillar of Islamic investing

What are Sukuk?

Sukuk are certificates of equal value that represent proportional undivided ownership in underlying Shari’ah-compliant assets or investments. They serve as an Islamic alternative to conventional bonds, adhering strictly to Shari’ah guidelines and requirements.

Differences between Sukuk and conventional bonds

| Characteristics | Sukuk | Conventional bond |

|---|---|---|

| Underlying Principle | Based on asset ownership and profit-sharing | Based on debt and interest payments |

| Compliance | Shari’ah-compliant (Islamic law) | Not subject to Shari’ah law |

| Returns to Investors | Profit or rent derived from assets | Fixed or floating interest (riba) |

| Ownership | Investors hold proportionate ownership in underlying asset/project | Investors are creditors, not owners |

| Use of Funds | Must be used for Shari’ah-compliant purposes | Can be used for any legal purpose |

| Risk Exposure | Linked to asset performance | Linked to issuer’s creditworthiness |

| Tradability | Tradable if asset-backed and Shari’ah-compliant | Freely tradable in most markets |

| Structure | Complex structures to ensure Shari’ah compliance | Straightforward debt instruments |

| Asset based | Generally asset-based | Usually unsecured or secured by general obligation |

| Regulatory Oversight | Financial institutions’ Internal Shari’ah Supervision Committee oversees regulations | Secular financial authorities |

Benefits of Sukuk

For investors:

- Shari’ah compliant

- Asset-based security

- Stable returns

- Portfolio diversification

For issuers:

- Access to Islamic capital markets

- Investor based expansion

- Infrastructure and development financing

- Flexibility in structure

Types of Sukuk

- Ijarah

Based on leasing; investors receive rental income from assets leased to a third party. - Murabaha

Based on cost-plus profit; the issuer sells an asset to investors at a marked-up price, with payments made over time. - Musharaka

A joint venture where both issuer and investors contribute capital and share profits and losses. - Istisna’

Used for construction or manufacturing projects; investors fund the building of an asset, which is delivered at a future date. - Mudarabah

A profit-sharing partnership where investors fund a business venture managed by the issuer, sharing profits per agreement.

Related resource

Click here to learn everything you need to know about Sukuk.

Glossary

For Glossary of terms, abbreviations and explanations on investments, please visit adcb.com/invglossary.

Wealth Management solutions

Discover reliable, innovative Wealth Management solutions. Learn more

Disclaimer

Abu Dhabi Commercial Bank PJSC is licensed and regulated by the Central Bank of the UAE. The Bank does not guarantee any providers, and investors invest at their own risk and bear all risks involved in any product purchased. The Bank will not be responsible for any investment decisions made based on this information. Past performance does not guarantee future results. Investment products are not bank deposits and are not guaranteed by the Bank; they are subject to investment risks, including possible loss of the principal amount invested. For Islamic Wealth Services Terms and Conditions please visit our website and/or to ADCB Asset Management Limited Terms and Conditions.